Let your Money not lose relevance with time

Let your Money not lose relevance with time

Savings Accounts

We get our money, probably a salary, in our bank accounts. This is often in a savings account (hopefully a salary account). The typical difference is that a salary account gives you the luxury of maintaining zero balance, whereas a regular savings account has a minimum balance requirement.

Now that the money has found its way to my account, what is the most you can do with it?

Satisfy the Instant Gratification Monkey – Spend it on products or services offering immediate returns (restaurant food, technology accessories, lifestyle buying, movies, travel). If you became richer during the Covid-lockdown, it means you often spend way too much in this bucket. Watching Netflix movies on Minimalism is a classic side-effect!

Spend on essentials – These include groceries, rent, fuel, phone bills, and all the other bills we have to pay the government. In the last decade, mobile connectivity has practically brought the world from six degrees of separation to one-two degrees of separation. That, unfortunately, did not translate to lesser travel. In what could be a silver lining around all the gloom, the Covid-lockdown has taught us what is possible. This bucket of spending is hard to lower – what each person defines as a necessity may be different, however it is a constant for that individual.

Money that sticks and stays in my account, maybe even grows just a little – Here we have a choice whether to let it be or let it grow. Every avenue to make my money grow is fraught with different levels of risks. Higher the returns, the higher the risk.

Expense Buckets

Every transaction you make will fall into one of these buckets. We will predominantly focus on helping you make the most of point 3. Using money to make money. But understand you need to make a conscious choice of how much of your monthly income is committed to each of these points. Most of us have very little idea about how much we pour into each of these buckets.

How to manage salary income?

The first step of change or analysis is to measure. So we suggest you look at your expenses for the past 3 months. Covid-lockdown will serve as a wonderful control to separate instant gratification expenses from essential expenses. For starters, I will share my expense here

Instant GratificationEssentialsSavingsPre-Covid Month26%39%35%Covid MonthClose to 0Stays SameProbably Goes Down (depending on you Income)

Our typical expense buckets

Please share your expense buckets in the comments below. Trust me, it is a worthwhile exercise!!

There could be a fourth point of actualization whether you spend money to buy a house (only if you are buying the house to stay in or earn rent for). If you are buying the house as an investment it again falls in expense bucket 3.

“Every time you spend money on buckets 1 or 2 remember you are taking it away from bucket 3. “

BUCKET 3: THE SAVINGS BUCKET

Lazy Money: You like to save, but have inertia to look for any instrument. So you let your money sit in the savings bank account. ICICI Bank– where most of us have salary accounts the returns are likely to be in 3 – 3.5% per annum (pa). Kotak Bank gives up to 6% pa and Bandhan Bank gives up to 7% pa.

A quick primer on how compound interest works.

Amount at the end of 5 years = Savings x (1 + Interest rate pa) x (1 + Interest rate pa) x (1 + Interest rate pa) x (1 + Interest rate pa) x (1 + Interest rate pa) …

For as many years as you might keep the money invested.

Let’s look at some numbers: if you invest INR 5000 on April 1, 2015, at 5% interest for 5 years, you will have 1700 on March 31, 2020. Instead, you spend it this year, and next year (April 1, 2016) when you have more money you actually invest 6000, then on March 31, 2020, you will actually have only 1657.

“Simple reason why you should start saving every little amount as soon as you can. “

If you leave the money in the bank, at least apples will be unaffordable.

If an apple cost 100 rupees in 2014, inflation (India numbers) will mean it will cost you 127 rupees in 2019. But 100 rupees in your savings account (at typical interest rate fluctuations) will reflect 134 rupees. This means you can just about manage your lifestyle by leaving money in the bank.

Like a see-saw precariously parallel to the ground, any change in your Bucket 3 on one side and Essential Expenses/Instant Gratification on the other side can send you to an uncomfortable unstable height; on the other hand filling your Bucket 3 will take you towards the safety of finding your feet on the ground.

If your essential expense goes up and your savings go down, spiralling into a vicious cycle. Eventually, you’ll need a higher paying job! That is the effect of so-called inflation. By design, saving accounts interest rates will only play catch-up with inflation.

And the best part of a savings account is it is just an ATM withdrawal away or as the jargon aficionados will call it – the investment is liquid.

A Savings Account is Barely Enough. Start Saving Today

Let’s say you have agreed to start making more money from your hard-earned money. How do you go down this path? What do you do first?

The single biggest thing you should do is understand how you might need money over the next 3 – 5 years. If you can define that, and often it takes time, then there is a different path you could take – a more comprehensive path looking at multiple investment avenues.

For today we are starting with the simplest – make money from your money instrument.

Your savings account:

When you open a bank account please pay attention to 2 things

What is the interest rate offered on money kept in the savings account?

What is the interest rate on money kept in Fixed Deposits (FDs)

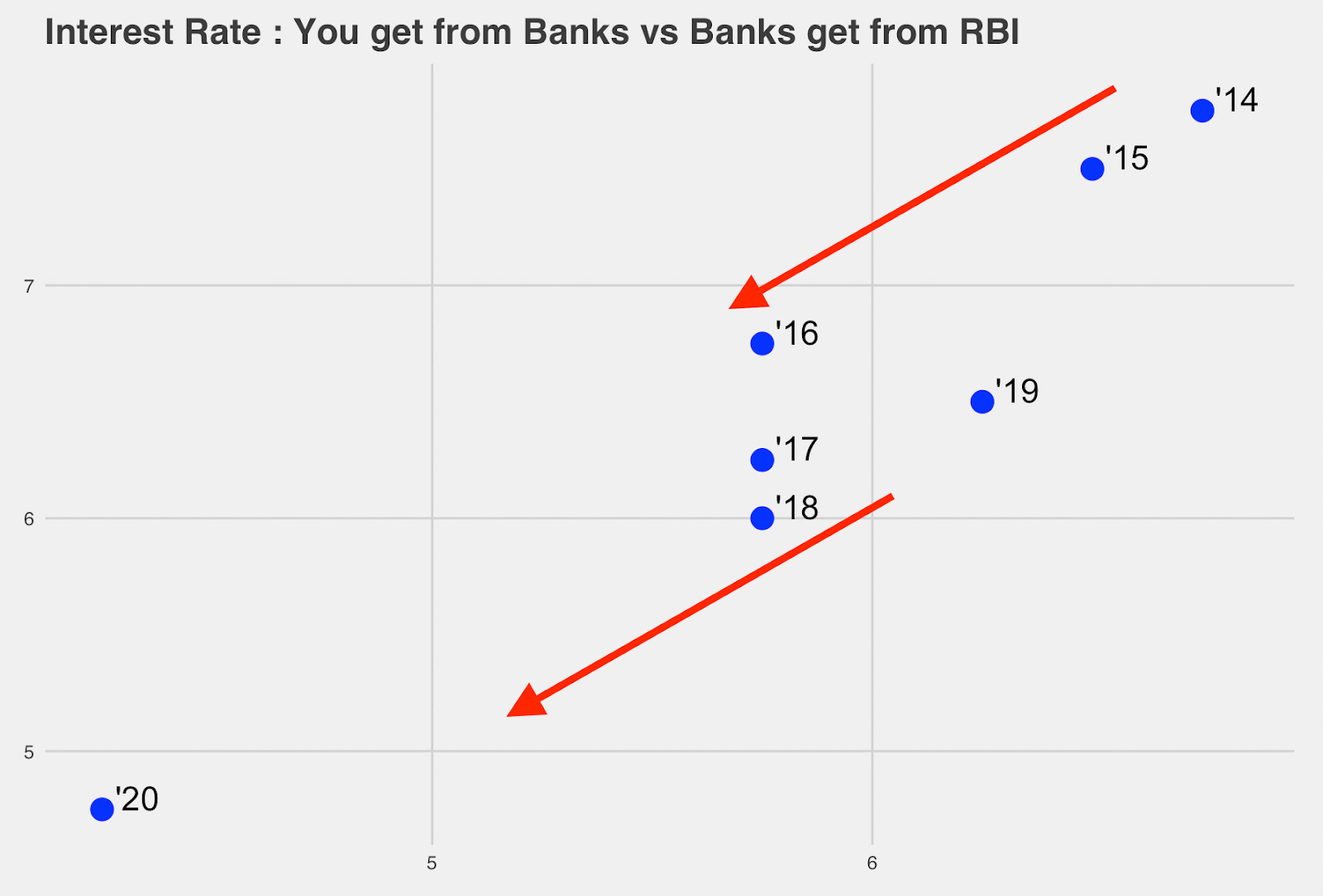

As of April 2020, the RBI has reduced reverse repo rates. Reverse repo rate is simply the interest rate at which RBI borrows money from banks like SBI, ICICI. This is RBI’s way of putting more or less money (more if the reverse repo is higher and vice versa) into the system. Banks react to this number and it is one of the levers of control with RBI. More interest means banks will increase the savings interest rate and money will infuse into the market resulting in higher inflation.

Currently safe to assume that whenever RBI reduces repo rate, Banks will reduce the interest offered on your savings accounts. But in recent years, Banks are giving a little less than they used to till 2016.

The first step you can do is look around for a new age bank and see if they are offering 6% p.a or more and probably make that your primary savings account. Given the debacle of Yes Bank, it is important to ensure the credibility of a Bank – read a bit of news about the bank before you finalize it.

This means that if you keep 1000 rupees in your ICICI savings account for 1 year, you will earn INR 30 or INR 35 at the end of the year. Historically (pre-2011) savings interest was calculated as the minimum amount kept in your account between the 10th of a month and the end of a month. Now however this is calculated daily.For example – they are offering up 7.8% returns per annum here (if you lock your investment for up to 40 months).

Thanks to some research for this article, I just created a small FD for myself on 24th April 2020. I recommend you explore doing this. It’s a completely online process. (No, these guys are not paying us anything!)

To give you some context – a typical FD gives you 6% per annum (today) – if you invest for a similar tenure, or even the 15 months FD in the above instrument gives better returns. So if your money is just sitting in your bank account you could put it here (maybe just INR 5000?). Now there is, of course, the argument around putting money in other instruments – another story for another day. But now that you have an FD offering you 7.3 – 7.5% returns per annum, you will need to look for assets/investments that can potentially give you higher returns. Or you can come back and put your money here.

If you other ideas on what to do with your money, share your comment.